Abercrombie & Fitch Co. (ANF) – Investment Research Report

This research paper explores Abercrombie & Fitch Co. (ANF) from an investor’s perspective, focusing on financial performance, valuation metrics, competitive positioning, and future price projections. The report includes a detailed analysis of ANF’s recent turnaround, economic moat, market trends, comparisons with industry competitors, and multiple valuation models. It concludes with 1-year and 2-year price targets supported by both quantitative and qualitative data.

Erik W.

4/23/202516 min read

1. Introduction

Abercrombie & Fitch, once known for its aspirational marketing and exclusivity, has redefined its brand to be more inclusive and digitally savvy. This transformation, driven by CEO Fran Horowitz, has revived its appeal and significantly improved financial results. The company has transitioned from a mall-based, image-driven retailer to a multi-channel, customer-centric operation focused on experience, relevance, and profitability.

This report examines the financial and strategic health of ANF, evaluates its relative valuation using various models (DCF, Graham's, and multiples), and compares it to industry peers. It is designed for long-term investors seeking a balanced approach between growth and value in the retail apparel sector.

2.Company Background

Founded in 1892, Abercrombie & Fitch Co. (ANF) has evolved from a niche outfitter of elite outdoor gear into a global retail powerhouse. Today, the company operates through three distinct lifestyle brands: Abercrombie & Fitch, Abercrombie Kids, and Hollister Co., each catering to different segments within the youth and young adult markets.

Abercrombie & Fitch targets older teens and young adults, focusing on casual luxury and timeless, elevated essentials.

Abercrombie Kids is designed for children aged 5 to 14, offering age-appropriate versions of the mainline brand’s styles.

Hollister Co., the most casual and trend-driven of the three, caters to high school and college-aged consumers seeking affordable, laid-back fashion with a Southern California aesthetic.

With more than 700 retail locations worldwide and a robust digital presence, ANF has effectively transitioned into an omnichannel retailer. E-commerce now contributes to over 40% of total net sales, driven by strategic investments in mobile optimization, data analytics, and direct-to-consumer logistics. The company has also expanded into key international markets, particularly in Europe and Asia, to diversify its geographic footprint.

In recent years, Abercrombie & Fitch has undergone a significant transformation of its brand. Moving away from its past reputation for exclusionary marketing, the company has adopted a new identity centered on social inclusion, body positivity, and authenticity. Campaigns now feature diverse models of different body types, ethnicities, and gender expressions, resonating with socially conscious Millennials and Gen Z consumers.

This rebranding initiative has not only modernized the company's public image but also revitalized consumer engagement and strengthened brand loyalty. By aligning with the values of a younger, more progressive audience, ANF is successfully redefining what it means to be a legacy brand in today’s dynamic retail landscape.

3.Financial Overview

Abercrombie & Fitch Co. (ANF) delivered a strong financial performance for the fiscal year ending January 2025, reflecting the successful execution of its strategic initiatives and the continued momentum of its brand revitalization efforts.

Key Financial Highlights:

Revenue: ANF reported total revenue of $4.28 billion, representing a robust year-over-year (YoY) growth of 16.5%. This increase was fueled by both physical store sales and significant gains in e-commerce, supported by targeted digital marketing and improved customer engagement across all three brand segments.

Net Income: Net income surged to $328.12 million, underpinned by disciplined expense management and top-line growth. This marks a significant shift from previous years and signals a return to sustainable profitability.

Earnings Per Share (EPS): The company reported diluted EPS of $10.71, marking a substantial improvement and reinforcing the effectiveness of its operational and strategic adjustments.

Gross Margin: Gross margin expanded to 63.1%, driven by improved inventory management, better full-price sell-through rates, and a notable reduction in promotional markdowns. These factors indicate a healthier product mix and more accurate demand forecasting.

Operating Margin: Operating margin rose to 12.4%, indicating increased operational efficiency and the positive impact of cost-saving initiatives across the supply chain and corporate structure.

Return on Equity (ROE): ANF achieved an impressive ROE of 47.35%, showcasing its ability to generate significant shareholder value through strong earnings and capital discipline.

Return on Assets (ROA): The company reported a ROA of 16.88%, indicating an efficient utilization of assets to generate profits, particularly notable given its physical retail footprint and investments in digital infrastructure.

Free Cash Flow (FCF): Free cash flow reached $392 million, providing ANF with the financial flexibility to reinvest in growth, repurchase shares, and reduce debt—actions that contribute to shareholder value and long-term economic stability.

Debt-to-Equity Ratio: The debt-to-equity ratio stood at 0.70, indicating a balanced capital structure and a manageable debt load. This reflects prudent financial management and a focus on maintaining liquidity while pursuing growth initiatives.

Shares Outstanding: The company had approximately 50.37 million shares outstanding, a relatively modest float that enhances the impact of earnings growth on shareholder returns.

Strategic Financial Insights:

Abercrombie & Fitch’s financial trajectory over recent years highlights a remarkable recovery from prior periods of underperformance. This rebound has been anchored by:

Margin Expansion through higher full-price sales and optimized sourcing.

Efficient Cost Control, including SG&A discipline and supply chain improvements.

Revenue Acceleration across all brands and geographies, driven by enhanced product relevance and omnichannel capabilities.

Consistent Growth in Free Cash Flow, allowing for strategic reinvestments, stock buybacks, and debt reduction without compromising operational agility.

Altogether, ANF’s financial results underscore a company that has not only stabilized but is now in a position of strength, ready to capitalize on future growth opportunities while delivering strong returns to investors.

4.Valuation Metrics

When compared to peers within the retail apparel industry, Abercrombie & Fitch Co. (ANF) appears undervalued, despite demonstrating superior profitability, operational efficiency, and a compelling growth trajectory. A review of key valuation multiples underscores the potential for upside re-rating, particularly as the company continues to execute on its brand transformation and capital return strategies.

Key Valuation Metrics:

Price-to-Earnings (P/E) Ratio:

ANF is currently trading at a P/E ratio of 7.81, which is significantly below the industry average range of 15–20. This valuation gap suggests the market has yet to fully price in ANF’s earnings strength and margin expansion, presenting a potential opportunity for multiple expansion as investor sentiment aligns with financial performance.Price-to-Book (P/B) Ratio:

The company’s P/B ratio stands at 3.00, indicating that the market values ANF at three times its book value. While slightly elevated compared to historical norms, this figure remains reasonable when viewed alongside the company's high return on equity (47.35%), which signals efficient capital utilization.Price-to-Sales (P/S) Ratio:

With a P/S ratio of 0.82, ANF trades at less than one times its annual revenue—another indicator of conservative valuation. This low ratio is particularly compelling in light of ANF’s consistent revenue growth and improving profitability, which are typically rewarded with higher sales multiples in the broader market.Enterprise Value to EBITDA (EV/EBITDA):

ANF’s EV/EBITDA multiple of 4.56 is markedly below the industry average. This metric, often used to assess a company’s value independent of capital structure, taxes, and depreciation, reinforces the view that ANF is trading at a discount relative to its underlying earnings power.Enterprise Value to Free Cash Flow (EV/FCF):

The company’s EV/FCF stands at 7.74, which is also on the low end compared to sector peers. Given ANF’s strong free cash flow generation ($392 million in FY 2025), this suggests that the market may be underestimating the sustainability and quality of its cash flows, especially important for funding strategic initiatives and shareholder returns.

Strategic Valuation Insights:

The combination of low valuation multiples and strong fundamentals presents a compelling investment case for ANF. The current discount may reflect lingering investor caution due to the company’s past volatility or broader sector headwinds. In sum, ANF represents a value opportunity within the retail space—one that could see meaningful multiple expansion in the near to medium term as the market recalibrates to reflect its operational transformation and earnings potential.

5. Economic Moat

Abercrombie & Fitch Co. (ANF) has a moderate but strengthening economic moat, driven by brand evolution, operational scale, and digital innovation. While not protected by a traditional luxury moat, ANF benefits from several soft competitive advantages that support long-term value creation.

Key Moat Drivers:

Brand Loyalty

ANF’s rebranding around inclusivity, body positivity, and authenticity has revitalized its image and deepened customer loyalty, especially among Gen Z and Millennials. High-quality, trend-forward merchandise further supports retention and engagement.Omnichannel Strength

Strategic investments in e-commerce, mobile apps, and direct-to-consumer logistics have enhanced customer experience, increased conversions, and strengthened global reach.Operational Scale

ANF’s global footprint and supply chain efficiencies provide cost advantages, enabling the company to compete effectively on both quality and price.Technology & Personalization

The use of AI and advanced analytics enhances product recommendations, inventory management, and marketing personalization, driving higher efficiency and a more tailored customer experience.

Summary: A Moat in Development

While ANF lacks an entrenched luxury position, its brand momentum, tech integration, and operational discipline form a durable set of soft moats. As these advantages accumulate, the company is well-positioned to sustain growth and withstand competition in the evolving retail landscape.

6. Competitive Landscape

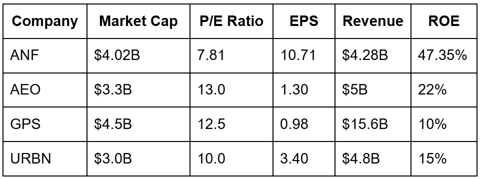

Abercrombie & Fitch Co. (ANF) operates in a highly competitive retail apparel environment, contending with both specialty retailers and fast fashion giants. Key competitors include American Eagle Outfitters (AEO), Gap Inc. (GPS), and Urban Outfitters (URBN). Each of these companies targets a similar demographic and competes across price, fashion relevance, and omnichannel capabilities.

Peer Comparison Snapshot

Key Takeaways:

Superior Profitability:

ANF leads its peer group in both Earnings Per Share (EPS) and Return on Equity (ROE). An EPS of $10.71 and ROE of 47.35% reflect the company’s strong operational efficiency, disciplined cost control, and effective capital deployment. This is especially noteworthy considering ANF’s revenue is lower than both Gap Inc. and American Eagle, yet its profitability is significantly higher.Valuation Advantage:

With a P/E ratio of 7.81, ANF trades at a significant discount to its peers, despite outperforming them on key return metrics. This undervaluation highlights the market’s conservative stance on ANF, offering potential upside as performance continues to improve and investor confidence builds.Efficient Capital Allocation:

Compared to competitors, ANF’s high ROE suggests it is generating more shareholder value per dollar of equity invested. This underscores better execution, strategic focus, and a leaner, more agile operating model.Scale vs. Efficiency:

While Gap Inc. remains the largest player by revenue, its relatively low EPS and ROE indicate lower efficiency and weaker margins. In contrast, ANF has optimized its size-to-profitability ratio, operating with fewer stores and lower revenue while delivering stronger bottom-line performance.

Conclusion: Competitive Strength Through Focused Execution

Abercrombie & Fitch is successfully carving out a competitive advantage in a crowded market through:

Strategic brand positioning

Operational discipline

Smart capital investment

Strong digital and omnichannel integration

As consumer expectations evolve and the industry continues to consolidate around digital capabilities and brand authenticity, ANF’s superior performance metrics position it as a standout player in the mid-tier fashion segment, capable of both growth and resilience.

7. Valuation Models

To estimate a fair value for Abercrombie & Fitch Co. (ANF), multiple valuation methodologies were employed, each offering a unique perspective on the company’s potential upside. The models include: Discounted Cash Flow (DCF), Graham’s Intrinsic Value Formula, Historical Multiple Analysis, and Peer Multiple Comparison.

a) Discounted Cash Flow (DCF) Model

The DCF model projects ANF’s future free cash flows and discounts them back to present value using a weighted average cost of capital (WACC). This model is particularly effective in capturing intrinsic value based on fundamental principles.

Key Assumptions:

2025 Free Cash Flow (FCF): $392 million

5-Year FCF Growth Rate: 10%

Terminal Growth Rate (beyond year 5): 2%

Discount Rate (WACC): 9%

DCF Outputs:

Present Value of 5-Year Cash Flows: ~$1.86 billion

Terminal Value (discounted): ~$3.65 billion

Total Enterprise Value (EV): ~$5.51 billion

Equity Value (after net debt adjustment): ~$5.2 billion

Intrinsic Value per Share: ~$172/share

Takeaway:

The DCF model reveals significant upside potential, indicating that ANF is materially undervalued relative to its cash flow generation capacity and long-term growth prospects.

b) Graham’s Intrinsic Value Formula

This formula, devised by Benjamin Graham, provides a simplified valuation approach by directly tying value to earnings and expected growth.

Formula:

Intrinsic Value = EPS × (8.5 + 2 × g)

Where:

EPS: $10.71

g (Expected Growth): 10%

Valuation:

$10.71 × (8.5 + 2 × 10) = $10.71 × 28.5 = ~$305.24/share

Takeaway:

Graham’s method yields a highly optimistic valuation, underscoring the potential upside if ANF maintains or exceeds its current growth trajectory. However, this model does not account for risk or capital structure and should be considered a bullish benchmark rather than a conservative baseline.

c) Historical Multiple Valuation

This approach values ANF based on its historical average P/E ratio, providing a reversion-to-the-mean framework for valuation.

Key Inputs:

10-Year Average P/E for ANF: 12

Normalized EPS (2025E): $10.71

Valuation:

12 × $10.71 = ~$128.52/share

Takeaway:

This method suggests that if ANF returns to its historical valuation multiple, the stock still offers meaningful upside from current levels. It reflects a conservative yet realistic valuation anchor.

d) Peer Multiples Valuation

Comparing ANF to its peer group helps assess relative valuation. Given ANF’s superior profitability and return metrics, applying the industry average P/E is justified.

Inputs:

Average Peer P/E (AEO, GPS, URBN): 12

ANF EPS (2025E): $10.71

Valuation:

12 × $10.71 = ~$128.52/share

Takeaway:

Even under a peer-based relative valuation model, ANF appears undervalued. Given its stronger fundamentals, the company arguably deserves a premium multiple, suggesting this may be a floor rather than a ceiling valuation.

Final Thoughts:

Each valuation model indicates substantial upside potential from current price levels. While Graham’s model presents the most bullish case, the DCF and multiples-based approaches offer more grounded benchmarks, all indicating that ANF is undervalued relative to its earnings power, free cash flow profile, and peer group.

8. Strategic Growth Initiatives

Abercrombie & Fitch Co. (ANF) is implementing a multifaceted strategy designed to sustain long-term growth, enhance profitability, and strengthen brand equity. The company’s initiatives are aligned with evolving consumer behaviors, environmental considerations, and global market opportunities.

1. Digital Acceleration

ANF is investing heavily in its digital infrastructure to meet the expectations of tech-savvy consumers:

Enhanced Mobile Experience:

Upgraded mobile apps now offer improved navigation, faster checkout, personalized product feeds, and integrated loyalty rewards.AI and Machine Learning Integration:

Algorithms tailor product recommendations and optimize search, driving higher conversion rates and increasing average order value (AOV).Omnichannel Integration:

Buy Online, Pick Up In Store (BOPIS), curbside pickup, and ship-from-store capabilities improve flexibility and efficiency.Social Commerce:

ANF leverages platforms like TikTok, Instagram, and Snapchat for direct shopping experiences, influencer-driven campaigns, and Gen Z engagement.

2. Store Optimization Strategy

Brick-and-mortar remains a vital touchpoint, but ANF is evolving its footprint to maximize efficiency and relevance:

Smaller, More Flexible Formats:

Transitioning from large, mall-based stores to smaller, community-focused layouts that better reflect local customer preferences.Pop-Up Retail:

Strategic pop-ups in urban and international locations test new markets and promote seasonal or exclusive collections.Flagship Store Enhancements:

Investments in high-traffic, brand-defining locations deliver immersive experiences and support marketing goals.Store Rationalization:

Closing underperforming stores to reduce overhead while reallocating resources to higher-growth regions.

3. International Expansion

ANF is actively pursuing global growth, particularly in Europe, Asia, and Latin America, where the brand is gaining momentum:

Localized Marketing Campaigns:

Tailored content and influencer partnerships that resonate with regional audiences.E-Commerce Expansion:

Investing in regional digital platforms and logistics to improve delivery speed and customer satisfaction abroad.Strategic Partnerships:

Exploring joint ventures and licensing deals to enter new markets efficiently and with reduced capital risk.Flagship International Stores:

High-profile openings in cities like London, Tokyo, and São Paulo are being made to build global brand equity.

4. Brand Repositioning and Marketing

ANF is redefining its brand identity to reflect the values of today’s youth:

Inclusive Campaigns:

Marketing focused on body positivity, gender inclusivity, and cultural diversity helps build emotional connections and trust with Gen Z and Millennials.Celebrity & Influencer Collaborations:

Capsule collections and social campaigns featuring micro- and macro-influencers increase brand reach and engagement.Content-Led Storytelling:

Emphasis on authentic narratives and real customer stories in advertising to enhance relatability and loyalty.Brand Portfolio Synergy:

Coordinated strategies across Hollister, Abercrombie Kids, and Abercrombie & Fitch ensure distinct brand voices while leveraging shared infrastructure.

5. Sustainability and ESG Initiatives

Environmental and social responsibility are at the core of ANF’s future strategy:

Carbon Neutrality Commitment:

Pledged to reach carbon neutrality across operations by 2030, with clear milestones for emissions reduction and offsets.Sustainable Materials:

Increased use of organic cotton, recycled fibers, and eco-friendly packaging materials.Water Conservation:

Innovations in denim production have led to significant reductions in water usage, targeting a 50% decrease in water consumption per garment.Supply Chain Transparency:

Partnering with ethically certified factories and providing traceability data to consumers.Community Engagement:

Initiatives supporting youth education, LGBTQ+ rights, and mental health awareness reflect ANF’s commitment to broader societal impact.

Summary:

ANF’s strategic roadmap strikes a balance between digital innovation, operational efficiency, international market expansion, and social responsibility. These initiatives position the company not only to capture near-term growth but also to evolve into a more agile, relevant, and future-ready brand in a dynamic global retail landscape.

9. Risks and Challenges

Despite its ongoing transformation and improving financial health, Abercrombie & Fitch Co. (ANF) faces several external and internal risks that could impact its operational performance, strategic goals, and valuation. Understanding these risk factors is essential for investors and stakeholders when assessing the company’s long-term prospects.

1. Economic Sensitivity

As a retailer in the discretionary consumer goods sector, ANF’s performance is closely tied to macroeconomic conditions:

Vulnerability to Economic Downturns:

During periods of recession or reduced consumer confidence, spending on apparel typically declines, directly impacting ANF’s revenue and profit margins.Inflation and Interest Rates:

Higher interest rates and inflationary pressures can reduce disposable income, while increasing ANF's input and operating costs, such as logistics, raw materials, and wages.Youth Market Exposure:

ANF’s core demographic—Gen Z and young Millennials—is more likely to be affected by job market instability, which could result in lower brand engagement during economic slowdowns.

2. Competitive Pressures

The global apparel industry is highly fragmented and intensely competitive, posing several strategic risks:

Fast Fashion Disruption:

Players like Zara, H&M, and Shein operate on faster production cycles, offering trend-responsive merchandise at lower price points.Direct-to-Consumer (DTC) Surge:

Emerging DTC brands leverage social media and influencer-driven models to bypass traditional retail structures, rapidly gaining market share and consumer mindshare.Price and Margin Pressure:

Competitive discounting can force ANF to offer promotions, which may erode gross margins and dilute brand equity.Innovation Gap:

A failure to maintain a pace of innovation, especially in tech, product, or digital marketing, could lead to a loss of relevance, particularly among trend-sensitive youth.

3. Foreign Currency & Geopolitical Risk

ANF’s expanding international footprint exposes the business to global market volatility:

Foreign Exchange (FX) Fluctuations:

Sales generated abroad, particularly in Europe and Asia, are vulnerable to currency conversion losses. A strong U.S. dollar can significantly reduce reported revenues and profits.Geopolitical Instability:

Trade restrictions, tariffs, and political uncertainty in key markets (e.g., China, Latin America) can disrupt supply chains, raise costs, or hinder expansion efforts.Operational Complexity:

Managing compliance, taxation, and legal frameworks across multiple regions adds administrative risk and increases overhead.

4. Fashion and Inventory Risk

The fashion industry is inherently cyclical and dependent on shifting consumer preferences:

Trend Misalignment:

ANF must accurately forecast styles and consumer demand across different demographics and regions. Missing a fashion trend can result in unsold inventory and costly markdowns.Seasonality:

Sales peaks are concentrated around back-to-school and holiday seasons, increasing the importance of precise inventory and promotional planning.Supply Chain Lag:

Lead times from design to shelf can leave ANF vulnerable to rapid trend changes, especially compared to fast-fashion competitors.

5. ESG and Reputational Risk

Environmental, social, and governance (ESG) issues are increasingly influencing consumer loyalty and investor decisions:

Sustainability Accountability:

Failure to deliver on stated goals around carbon neutrality, ethical sourcing, or water conservation could lead to consumer backlash and negative media attention.Labor & Supply Chain Ethics:

Any exposure to unethical labor practices, particularly in outsourced manufacturing, can lead to reputational damage and regulatory scrutiny.Greenwashing Concerns:

Investors and consumers are becoming more discerning; overstating ESG achievements without measurable progress may be viewed as misleading or insincere.Brand Legacy:

While the company has rebranded itself around inclusivity, past controversies or public missteps could resurface and reignite criticism.

Summary:

ANF’s strategic positioning and financial momentum are promising, but the company remains susceptible to a variety of risks ranging from economic cycles to fashion volatility and ESG-related accountability. Proactive risk management, scenario planning, and continued innovation will be crucial in navigating these challenges and sustaining long-term shareholder value.

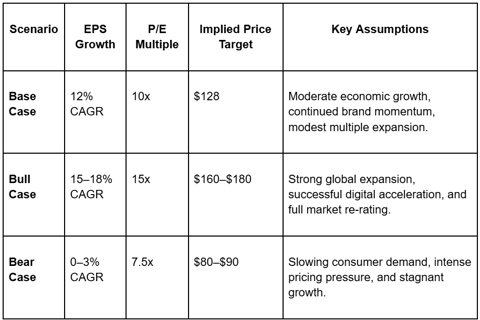

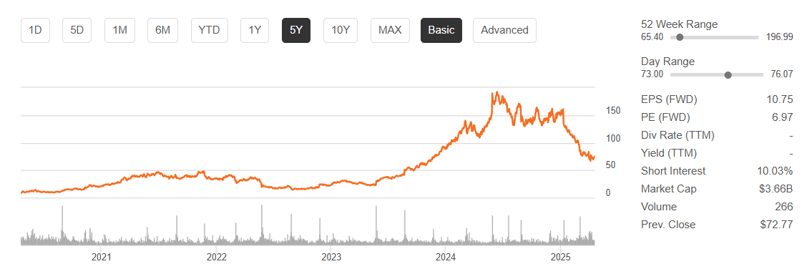

10. Price Target Analysis

To assess the potential upside for Abercrombie & Fitch Co. (ANF), we’ve conducted a multi-scenario analysis that incorporates earnings growth assumptions and valuation multiple expansion. The projections take into account both internal performance drivers and external market conditions.

Scenario-Based Valuation Outlook

1-Year and 2-Year Price Targets by Blackworth & Co.

Based on ANF’s improving fundamentals, strong brand recovery, and valuation re-rating potential, Blackworth & Co. assigns the following price targets:

1-Year Price Target: $125

This target is based on a modest P/E expansion to 10x forward earnings, assuming continued double-digit EPS growth driven by operational efficiency, margin expansion, and sustained e-commerce performance.2-Year Price Target: $160

This longer-term target reflects ANF achieving a bull-case scenario, with EPS compounding at 15–18% annually and investor sentiment lifting the P/E multiple to ~15x, on par with or above historical averages and closer to peer valuation norms.

Key Catalysts Supporting Target Upside

Margin Expansion: Continued improvements in gross and operating margins through better inventory management and cost controls.

Digital and International Growth: Increased penetration in e-commerce and emerging markets is boosting topline performance.

Multiple Expansion Potential: With ANF currently trading at a forward P/E of approximately 7.8x, which is well below the retail industry average of 15–20x, there is significant room for a valuation re-rating.

Free Cash Flow Strength: Robust free cash flow generation provides capital for share buybacks, thereby reducing the share count and enhancing EPS growth.

Positive Sentiment Shift: Rebranding success, influencer campaigns, and improved ESG credentials are driving customer and investor goodwill.

Downside Risks to Monitor

Consumer Pullback: A slowdown in discretionary spending could hinder top-line growth.

Valuation Ceiling: If sentiment remains skeptical, the multiple may stay compressed despite operational improvements.

Execution Risk: Missteps in product strategy, digital experience, or international expansion could stall growth momentum.

Summary

ANF offers compelling upside potential under both base and bull-case conditions. The stock’s current valuation appears to be disconnected from its improved earnings quality, making it an attractive opportunity for both growth-oriented and value-focused investors. Blackworth & Co.’s price targets of $125 in 12 months and $160 over two years reflect a high level of conviction in the company’s turnaround story and ongoing strategic execution.

11. Conclusion

Abercrombie & Fitch Co. (ANF) has successfully transformed from a legacy mall-based retailer into a modern, omnichannel lifestyle brand with a distinctive market presence. Through strategic rebranding, operational improvements, and a renewed focus on customer-centric values such as inclusivity and authenticity, the company has reestablished its relevance with Gen Z and Millennial consumers—core demographics that are shaping the future of retail.

On the financial front, ANF has delivered a robust performance, marked by accelerating revenue growth, expanding margins, and significant improvements in return metrics such as ROE (47.35%) and ROA (16.88%). The company’s enhanced free cash flow generation and prudent balance sheet management—highlighted by a sustainable debt-to-equity ratio of 0.70—further strengthen its investment profile.

Valuation models consistently suggest that ANF is undervalued relative to both its historical averages and industry peers. With a forward P/E ratio of just 7.81, the stock trades at a substantial discount despite superior earnings quality and return on equity. Across multiple methodologies—including discounted cash flow (DCF), historical multiples, and peer comparisons—the stock shows upside potential ranging from 30% to over 50% within a 1–2 year investment horizon.

Strategically, the company is well-positioned to capitalize on several long-term growth drivers:

Digital acceleration and AI integration fueling e-commerce sales and personalization.

International expansion into high-potential markets like Asia and Latin America.

Store portfolio optimization boosting profitability.

Sustainability and ESG initiatives enhancing brand equity and stakeholder trust.

At the same time, ANF is demonstrating disciplined execution in navigating risks associated with macroeconomic uncertainty, fashion cycles, and industry competition.

Investment Thesis Summary:

Strong Brand Momentum: A revitalized brand that resonates with modern consumers.

Operational Efficiency: Industry-leading ROE and margin expansion.

Attractive Valuation: Trading well below intrinsic and relative value estimates.

Strategic Growth Pipeline: Multiple levers for long-term value creation.

Final Verdict:

Given ANF’s improved fundamentals, discounted valuation, and clear strategic direction, the stock presents a compelling opportunity for investors seeking mid-term capital appreciation. For those with a 1–2 year horizon, ANF offers a favorable risk/reward profile backed by solid execution, brand strength, and upside re-rating potential.

References:

StockAnalysis.com. (n.d.). Abercrombie & Fitch Co. (ANF) financials and stock metrics. Retrieved April 23, 2025, from https://www.stockanalysis.com/stocks/anf/

Macrotrends. (n.d.). Abercrombie & Fitch (ANF) financial ratios and data. Retrieved April 23, 2025, from https://www.macrotrends.net/stocks/charts/ANF/abercrombie-fitch/financial-ratios

FullRatio. (n.d.). Abercrombie & Fitch Co. (ANF) key financial metrics and valuation. Retrieved April 23, 2025, from https://www.fullratio.com/stocks/nyse-anf

AlphaSpread. (n.d.). ANF intrinsic valuation and DCF model. Retrieved April 23, 2025, from https://www.alphaspread.com/security/nyse/anf/summary

Yahoo Finance. (n.d.). Abercrombie & Fitch Co. (ANF) stock summary and news. Retrieved April 23, 2025, from https://finance.yahoo.com/quote/ANF/

Bloomberg. (n.d.). Abercrombie & Fitch Co. financials and stock data. Retrieved April 23, 2025, from https://www.bloomberg.com/quote/ANF:US

Abercrombie & Fitch Co. (2024). Form 10-K Annual Report for the fiscal year ended January 2024. U.S. Securities and Exchange Commission. Retrieved from https://investor.abercrombie.com/

Investopedia. (n.d.). Financial ratio analysis and valuation methods. Retrieved April 23, 2025, from https://www.investopedia.com/

The Times. (2024, December 5). Abercrombie & Fitch finds new life with Gen Z revival. The Times UK. Retrieved from https://www.thetimes.co.uk/